January 27, 2022

Maine’s 2022 Capital Markets Outlook:

GENERAL TRENDS

In last year’s Market Outlook, we stated that given the savory ingredients of abundant liquidity, low cost of capital, wider yield spreads, and rebounding asset value appreciation, we expected investor appetites to acquire more commercial real estate (CRE) in 2021 to return to the insatiable pre-COVID levels, albeit with some sectors faring better than others. As of late 2021, this prediction has proved accurate, with a number of assets commanding multiple bids and trading at record low cap rates – especially in the industrial sector. However, the rapid surge of inflation is the specter of doom lurking as we cast our eye to 2022. How the monetary authorities respond will in part dictate whether CRE’s unprecedented bull run will continue.

Often in these inflationary times, trade publications and cocktail parties are dominated by statements such as “real estate is a good hedge against inflation” and “inflation drives investors towards commercial real estate.” While there is an element of truth in this sentiment, an investor should be wary in these volatile times and consider what makes the CRE investment appealing as opposed to other investment options available.

Simplified: high inflation rates typically cause the Federal Reserve System (Fed) to raise interest rates. When interest rates are higher, it becomes more expensive to borrow money. Many real estate investors use debt to purchase assets, and this increase in cost of debt can lead to decreased returns to the investor – thus depressing the price attainable by a seller, which results in a higher cap rate. However, the question today is whether the Fed views inflation as permanent. If it does the latter, you can expect a distinct rise in interest rates, which will impact CRE negatively in the short term (next 12-24 months).

Assuming a stable interest rate environment, inflation can benefit CRE owners if there is strong demand and lease structures favorable enough to take advantage of rising rental rates. However, inflationary pressures will impact performance on the operating expense side. Senior housing, assisted living/memory care, and hospitality are the most labor intensive sectors and impacted the most by surging inflation. Furthermore, multifamily and industrial generally tend to outperform on a risk-adjusted basis in an inflationary environment, as rents have been increasing and demand has stayed consistent.

The other variables that we need to consider as we forecast capital markets behavior are changes to trade policy, taxation, discretionary spending, housing, education, healthcare, and government regulation – all of which will impact commercial real estate. President Biden recently signed the $1.2 trillion infrastructure bill passed by Congress, with plans to push forward with an additional $2 trillion social spending bill. Within the American Families Plan, there is a proposal to limit 1031 “like-kind” exchanges commonly used by CRE investors to reinvest proceeds from the sale of real estate. The 1031 exchange accounts for 10% to 15% of annual CRE transactions, so we can expect a correlation in CRE transaction volume reduction should the exchange provision be modified or eliminated. It is interesting to note that we saw a flurry of activity in Q4 of 2021 with sellers motivated to close before end-of-year to avoid the unknown of tax policy in 2022.

Analyzing CBRE’s US Capital Markets publication through Q3 of 2021, we saw that total capital markets investment volume in 2021 was up 19% year-over-year (YoY) and it was predicted that global investment volume would reach 23% by year end.

Despite the inflationary environment forecast for 2022, we expect the appetite to acquire commercial real estate to remain strong, albeit with some sectors faring better than others.

LOCAL TRENDS

Traditionally, Maine has been a stable market, somewhat resistant to the volatility that the rest of the country experiences. Employment statistics returned to pre-COVID normal and with inexpensive capital available, we expect steady demand for investment property statewide in 2022. While we expect that interest rates will increase moderately in 2022, cap rates will remain stable in most markets and sectors. Industrial and multifamily buildings continue to trade in the lowest cap rate range. We anticipate that long-term fixed debt and historically low rates will continue to be available in Q1 and Q2 of 2022. There also continues to be a steady mix of out-of-state capital and local buyers demanding product throughout the State of Maine. We have also seen a high level of interest in mixed retail-industrial properties that we expect to continue.

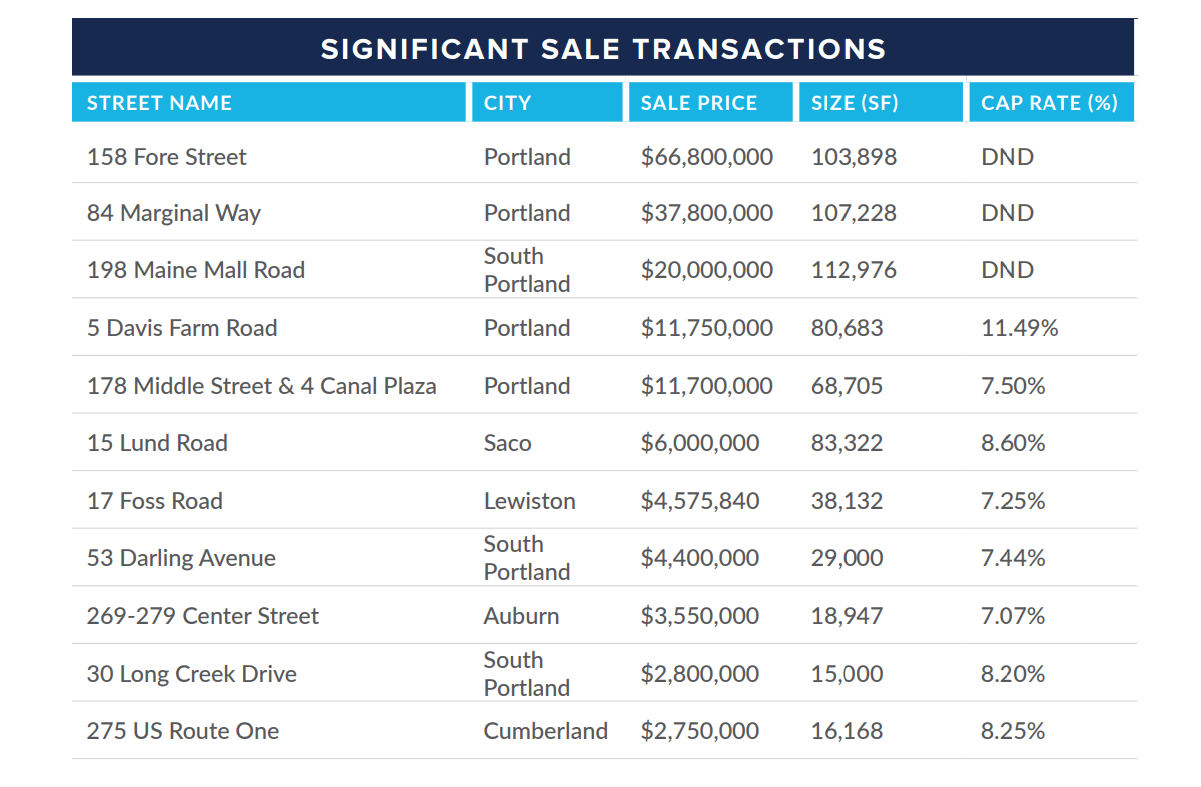

The Boulos Company facilitated more than $237 million in transactions on behalf of clients in 2021. Over $54 million of that volume represents investment sale transactions. The industrial sector alone accounted for over 22% of the total sale transaction volume at just under $28 million.

In conclusion, in the lead-up to year-end 2021, we are seeing a higher number of investors exploring disposition versus refinance scenarios than in years past. Therefore, we expect there to be more availability of investment product in 2022 than this past year. We expect robust activity in the first and second quarter, with investors capitalizing on late-cycle market dynamics. The Boulos Company looks forward to working with you to develop and execute your real estate strategy in 2022.

Chris Paszyc, CCIM, SIOR Partner, Broker