January 27, 2021

Industrial Market Update: 2021

Jon Rizzo, Broker

Originally Featured in our 2021 Greater Portland Market Outlook.

The 2020 overview of Maine’s industrial market looks a lot like 2019’s—strong tenant demand, lack of supply, and an incredibly sought-after investment market. But there is one notable difference. Demand increased even more in 2020, due to COVID-19.

Before diving into the Greater Portland market, let’s look at the industrial sector on a national level, as many of the fundamentals in the overall U.S. market hold true for Maine. Much of the demand for industrial properties in 2019 was e-commerce driven. This trend is likely to continue, as consumers have embraced online shopping during the pandemic, and with COVID-19 continuing to be a factor through the first half of the year.

According to CBRE Research, “$1 billion in incremental e-commerce sales generates 1.25 million sq. ft. of warehouse space demand.” So the increase in e-commerce sales will naturally lead to an increase in demand, and with vacancy rates being so low, new construction is inevitable. New construction typically yields a higher lease rate, which trickles down to higher lease rates for second and third generation inventory as well. The increase in overall lease rates strengthens the landlord market but hasn’t seemed to slow tenant demand.

Are speculative projects on the horizon? The consensus answer is “yes” as, according to CBRE Research, there was strong pre-leasing of speculative development in Q3 of 2020. On a macro level, this trend in new construction and demand for more industrial space does not seem to be slowing down in 2021 and is, in fact, projected to increase. The question becomes when do we hit the lease rate tipping point for tenants, given developers’ yield expectations and corresponding construction costs and ultimate deal terms (length of term, tenant improvement allowance, lease rate, etc.)

How does this relate to the market here in Greater Portland? Let’s look at the numbers.

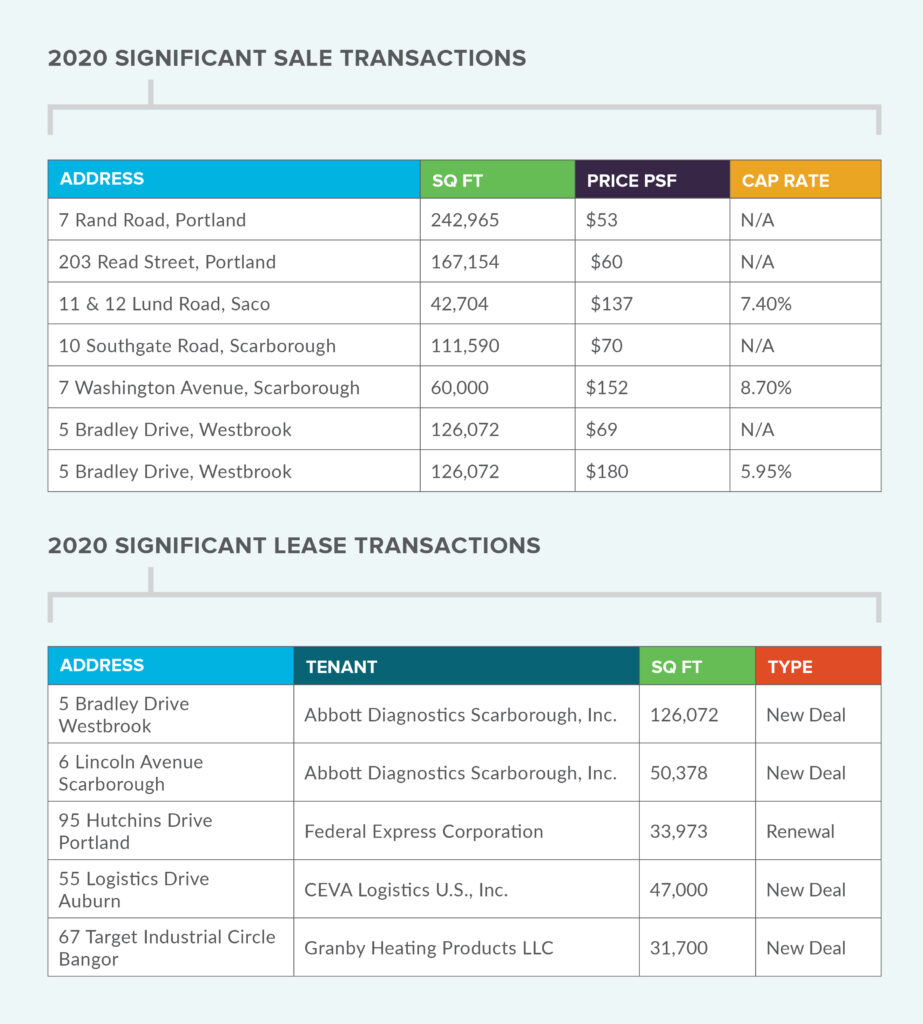

We are currently experiencing a vacancy rate that is approximately 2.5%. With nearly 20 million square feet of inventory, this translates to 500,000± SF. There is a significant vacancy at 203 Read Street in Portland (167,000± SF) that represents approximately 33% of the available vacant space. According to the listing brokers at NAI The Dunham Group, they are in negotiations with tenants to lease roughly 150,000± SF in that building. If you take 203 Read Street entirely out of the equation, the vacancy rate drops down to 1.7%. Clearly, we are experiencing an extremely tight market.

In Scarborough, 65% of the light industrial lots in Phase 1 and Phase 2 at the Innovation District at The Downs are under contract or sold, with a few buildings already constructed and occupied. Several others are under construction, breaking ground, or planned and likely to be completed by spring/summer 2021. This type of activity has taken place within 16 months of the official ground breaking at the Innovation District. Many of the end-users had been considering existing inventory, but the lack of quality product and higher asking prices for existing buildings has led to new construction.

Not All About Lack of Supply

Of course lack of supply plays a role in new construction for end-users/tenants. However, it is also about building specifications and what can or can not be met with an existing building and potential fit-up. Tenants are seeking higher quality assets—newer product, greater clear height, more efficient column spacing, better trailer access (docks, overhead doors, parking, turnaround, etc.), and location. And they’re willing to pay a premium for these specifications. When a property with A+ characteristics hits the market, it draws attention from any and all tenants in that market and does not stay listed for long. Larger scale assets of this type also draw attention from the capital markets (typically 50K square feet and greater with investment grade tenants).

Looking Forward

So what do we see happening in 2021? The vacancy rate will hover in the same range that we’ve seen the last two years—between 2% and 3%. There are a few larger buildings that are being marketed for build-to-suit projects and likely will not break ground without the majority of the building having a commitment from a tenant. Even if those projects were built on spec they would not be completed until Q4 2021 at the earliest, thus not affecting the vacancy rate for most of the year.

Consumer e-commerce demand will continue and likely increase during Q1 and Q2 of 2021 with the effects of COVID-19 still very much upon us. In order to keep up with this demand and increase efficiency, companies are going to need to streamline delivery to keep costs down and keep customer satisfaction high. This will increase demand for “final mile” distribution centers. Consistent with the national outlook, the Greater Portland market has a lack of existing inventory, and this should continue to drive new construction and/or lead to adaptive reuse of existing buildings. Think retail to industrial. With traditional brick and mortar retail struggling, in particular big box retailers, we’ve seen adaptive reuse of these spaces as warehousing and distribution. Big box retail stores are typically located in densely populated areas—the ideal location for a final mile distribution center. The question becomes, does zoning allow for this type of use, and if not, can the ordinance be amended? This is a great reuse of a vacant/obsolete box store and municipalities should welcome this type of conversion.

Consumer e-commerce demand will continue and likely increase during Q1 and Q2 of 2021 with the effects of COVID-19 still very much upon us. In order to keep up with this demand and increase efficiency, companies are going to need to streamline delivery to keep costs down and keep customer satisfaction high. This will increase demand for “final mile” distribution centers. Consistent with the national outlook, the Greater Portland market has a lack of existing inventory, and this should continue to drive new construction and/or lead to adaptive reuse of existing buildings. Think retail to industrial. With traditional brick and mortar retail struggling, in particular big box retailers, we’ve seen adaptive reuse of these spaces as warehousing and distribution. Big box retail stores are typically located in densely populated areas—the ideal location for a final mile distribution center. The question becomes, does zoning allow for this type of use, and if not, can the ordinance be amended? This is a great reuse of a vacant/obsolete box store and municipalities should welcome this type of conversion.

Greater Portland’s industrial sector is going to continue to grab attention from local and regional investors due to the fact that it has been largely unaffected by COVID-19 compared to sectors such as office and retail. With strong market fundamentals, we are seeing cap rates trending closer to those of larger markets, such as Boston and New York, but providing a spread that makes investing in Greater Portland more attractive than those markets.

Download The Full Market Outlook