January 13, 2022

Office Market Overview: 2022

The Greater Portland Office Market has remained resilient over the past couple years, as evidenced in our survey last year. We had all hoped for a return to some normalcy in the office market in 2021, but as the pandemic continues, so does the uncertainty of its impact on office space. Here at The Boulos Company, we didn’t know what to expect from our annual Office Market Survey this year. How were office occupiers, large and small, going to use their offices moving forward? Did they still even need them at all? Through our COVID Office Impact Survey, we found that, yes, offices are still needed, and the data pulled in our 2022 Greater Portland Office Market Survey supports that. The question went from “Do we need our office?” to “How do we use our office?” Despite a year plagued by uncertainty and change, the market proved surprisingly strong and, while demand has stayed moderately low, vacancy rates were kept in check this past year.

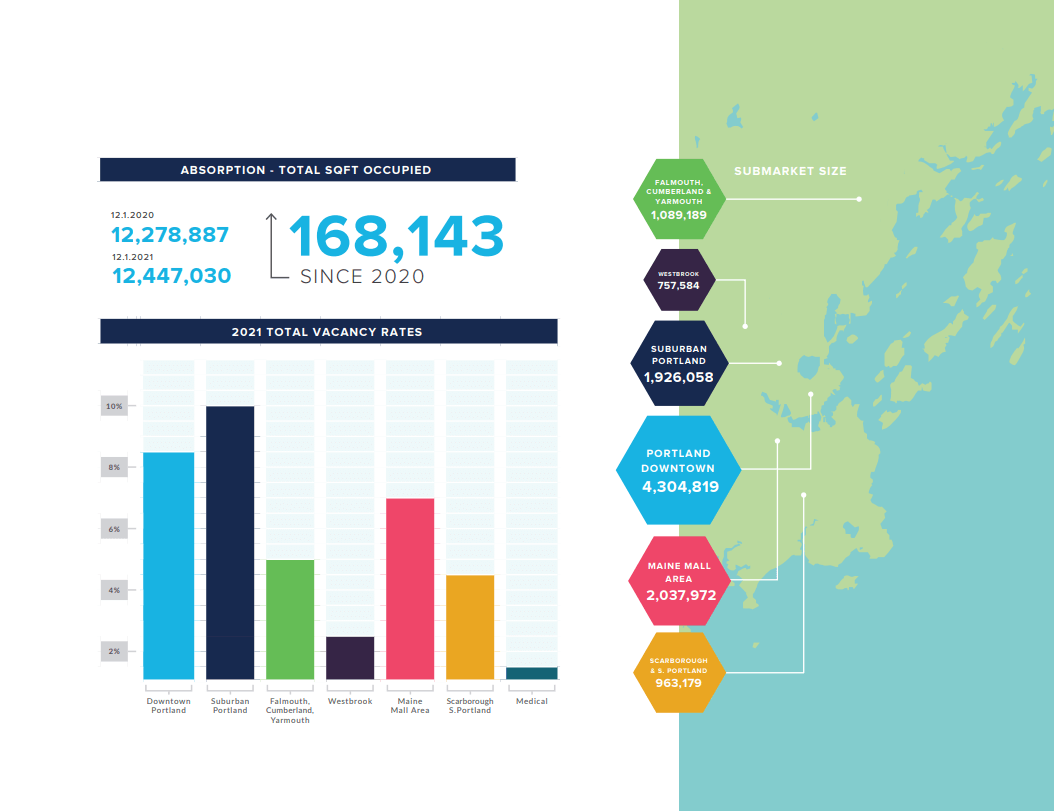

As of December 1, 2021, the direct vacancy rate fell to 6.73% across the entire Greater Portland market. This is down slightly from 6.97% in 2020 and shows that, despite the ongoing pandemic and reevaluation of the office space, there was not much movement in the direct rate – a surprise to many. However, what was anticipated was a continued increase in sublease space being offered. This rate increased from 1.73% in 2020 to 2.70% in 2021 with 125,000± SF of sublease space added over the previous year. This increase in the sublease rate pushed the total vacancy rate to 9.42% in 2021, an increase from a total rate of 8.70% in 2020.

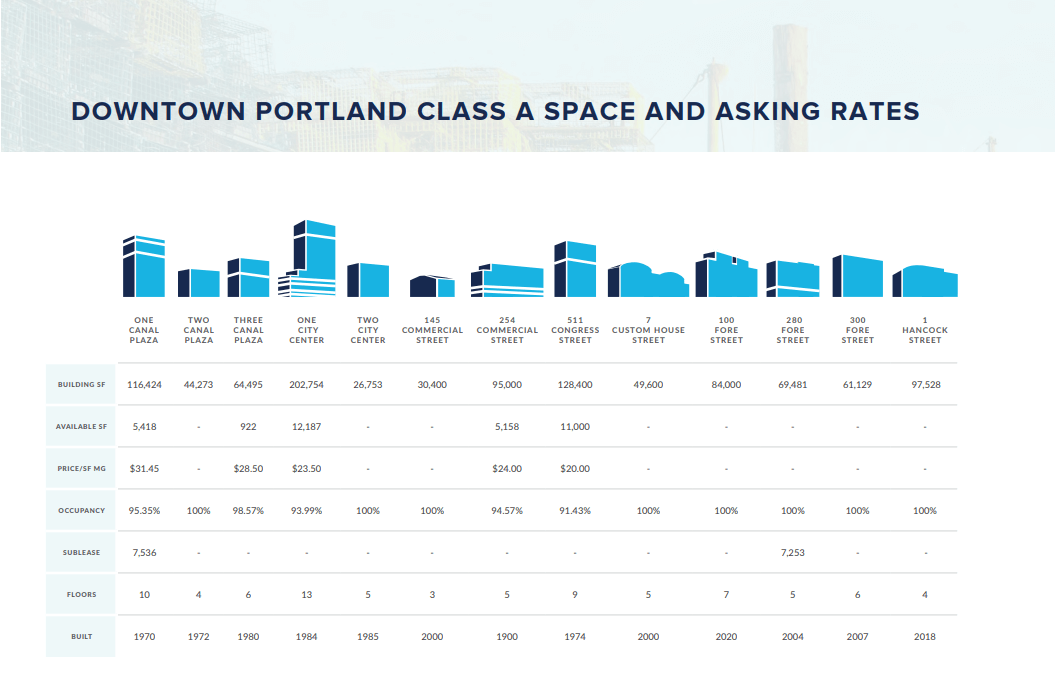

Downtown Portland

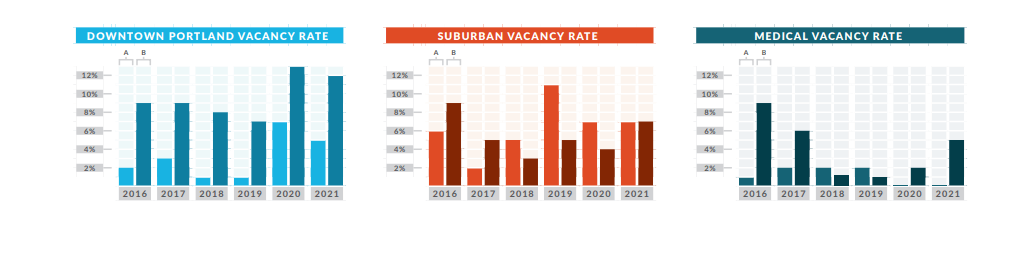

After a spike in the overall downtown vacancy rate in 2020, rates rebounded in 2021. The direct vacancy rate for both Class A and Class B markets fell to a collective 8.61%. This is still the highest rate since 2013, but nowhere near the height of the downtown vacancy rate of 13.96% in 2011. The sublease rate remained relatively unchanged from the year prior. The downtown Class A market, which had a direct vacancy rate of just 0.61% only a couple years ago, fell from 6.60% in 2020 to 5.02% in 2021. This is largely due to one significant transaction, as the University of Maine leased 61,000± SF of vacant office space for The School of Law and Maine Graduate & Professional Center. This market is also poised for continued growth with the new Covetrus and Sun Life buildings slated to open in 2022.

Along with the Class A market, the downtown Class B vacancy rate also dropped, falling from 13.32% in 2020 to 12.29% in 2021. No large leases were signed in this market to push the rate lower, however, the drop can be attributed to numerous smaller transactions and a trend in Class B buildings being converted from vacant office space to residential and hospitality uses. Over the last half decade, close to 200,000 square feet of Class B office space, much of it vacant, has been removed from our survey.

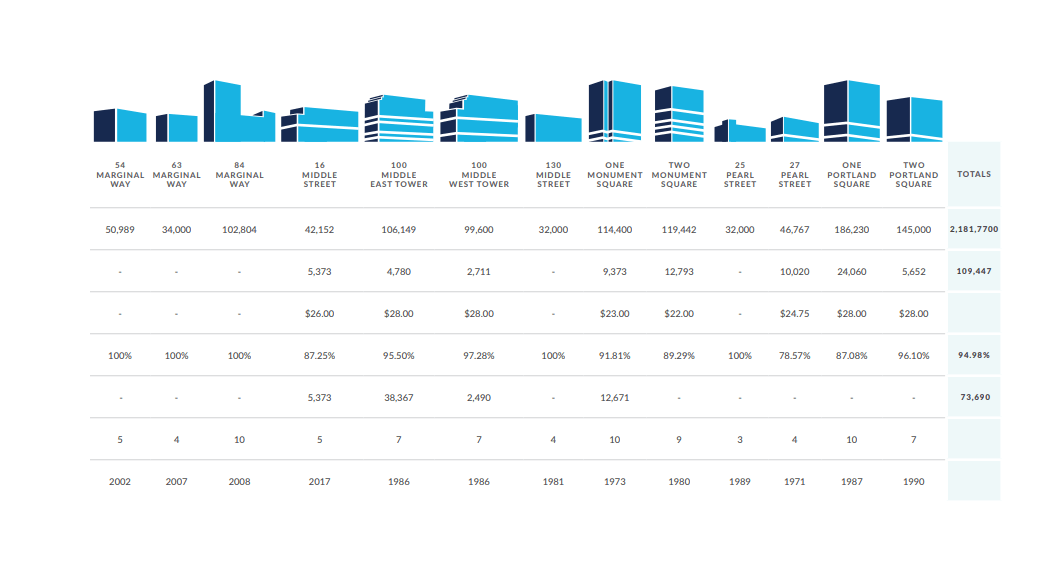

Suburban Office

While the overall and downtown markets experienced a drop in the direct vacancy rates, suburban Class A and Class B rates increased slightly from 6.29% up to 6.67%. This remains a healthy rate compared to years past, lower than any year from 2009 until 2014 during the Great Recession. The suburban markets consist of South Portland, Scarborough, Maine Mall Area, Westbrook, and Falmouth/Cumberland/Yarmouth. There was an increase in vacancy at some level across all submarkets except for Class A properties in the Maine Mall area and Class B properties in the Falmouth/Cumberland/Yarmouth market.

Despite the overall increase in suburban rates, Class A properties had a decrease in the vacancies from 7.04% down to 6.57%. This was largely driven by significant transactions in the Maine Mall area, especially the leasing of 34,000± SF at 65 Gannett Drive and 31,000± SF at 225 Gorham Road. However, the aforementioned increase in sublease space on the market is almost entirely concentrated in the Maine Mall area, with considerable vacancies on the horizon in this market over the next three years. This may have a sizable effect on vacancy rates, given the current demand for office space in these markets.

The suburban Class B vacancy rate saw one of the largest changes in any market. The vacancy rate rose to 6.85%, up from 4.84% in 2020, and serving as the driver behind the increase of suburban rates overall. Once again, the influence behind this change was concentrated in the Maine Mall area, as the Class B rate in this submarket increased from just 3.86% to 11.95% over the past 12 months. Most other Class B submarkets experienced an increase in vacancy rates, although most were relatively minor.

Medical Office

Despite the pandemic, medical office space rates remain historically low, although there was a slight increase in this submarket for the first time in several years. This increase was from just 0.52% in 2020 to 1.11% in 2021, still an extremely low rate in a market that experiences very little turnover. Added to the survey this year was 92 Campus Drive, a 108,000± SF medical building on the MaineHealth campus in Scarborough. The 62,000± SF VA outpatient clinic on Commercial Street will be occupied in the early part of 2022 and will be included in next year’s survey.

2022 Office Market Forecast

Last year’s forecast was not easy, and this past year did not make the future much clearer. We were right in assuming that there would not be a snap back to pre-pandemic rates and that the overall market may remain relatively unchanged. For 2022, we may experience much of the same, as the office market is still in flux. The pandemic may eventually have a more significant impact on the market, but we did not see it this year, and there are no obvious signs to a mass exodus of office space. While the amount of sublease space on the market is concerning, it is unlikely that this will have a major effect over the next 12 months. Additionally, there are several transactions underway that will only improve the overall rates. A return of demand for office space is important to market absorption, and the recovery has proved slower than initially anticipated. However, over the past two years, we have all learned to adapt – the office market is no different.

Nate Stevens, Partner, Broker